Tech

“Man in the Fog” – The Story Enshrouding Google and the Race to Find Solutions: How to Make Money Beyond Advertising?

As it approaches its 25th anniversary, Google, the “middle-aged” titan, is ardently pursuing avenues to rejuvenate its identity.

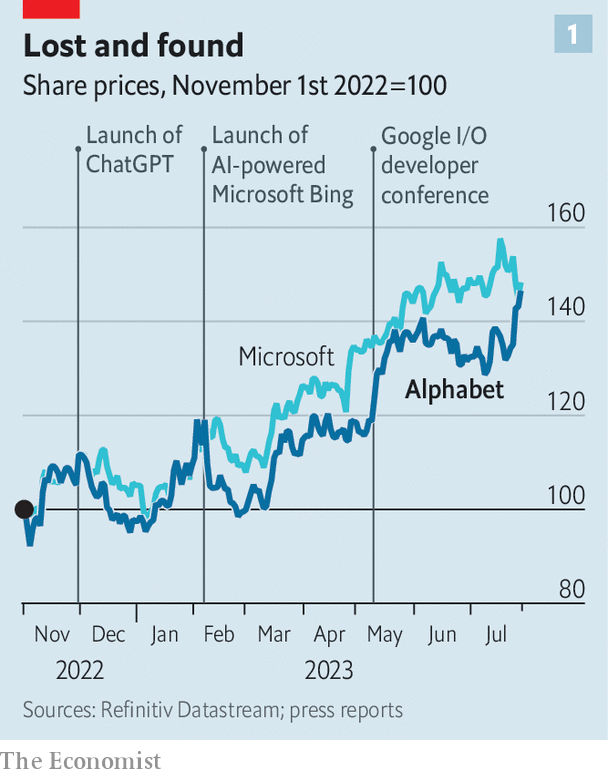

In November last year, a strange event occurred in Mountain View, USA. A dense “fog” covered the headquarters of Alphabet, the parent company of Google. This “fog” referred to ChatGPT – an artificial intelligence language model created by OpenAI, a startup backed by Microsoft. ChatGPT caused panic throughout Alphabet’s headquarters.

ChatGPT provided human-like answers to the questions users asked, even answering the crucial questions that power Google’s lucrative search engine. In February, OpenAI and Microsoft released an advanced version of the Bing search tool – a move believed to directly challenge Google’s “lunch.”

Eight months later, the fog had almost dissipated. On July 25th, the company reported robust quarterly results. Revenue increased by 7% compared to the same period last year, reaching $75 billion USD. They continued to generate substantial cash flow: In the 12 months ending in June, the company made $75 billion USD in operating profit. Bing showed no noticeable impact on Google’s global monthly search query market share – the company still holds over 90% of the market share.

Most importantly, Google has extinguished any perception that they have fallen behind in technology. In May, Sundar Pichai, the CEO of both Google and Alphabet, revealed over a dozen AI-powered products at I/O, an annual event for software developers. These products included AI tools for Gmail, Google Maps, and Google Cloud. Investors felt reassured, especially after Bard, Google’s chatbot, was hastily launched in February and encountered numerous errors. Since then, the company has rolled out other AI products and features. On July 12th, they introduced NotebookLM, an AI-powered note-taking tool trained on user documents.

On the same day, Nature, a scientific journal, published a paper by Google researchers describing an AI model that matches human doctors’ responses to questions about appropriate treatment methods for patients. A day later, they updated the Bard version with fewer bugs, mastering more than 40 human languages and over 20 computer languages, and launched it in the EU. A tool codenamed Gemini, aimed at taking down ChatGPT, is in progress. After falling below $1 trillion in November, Alphabet’s market value has rebounded to $1.7 trillion.

But has the crisis passed?

In the short term, the answer is likely yes. However, like all moments of extreme anxiety, the panic over one chatbot company raises broader questions: What is the current state of one of the world’s largest companies, and what does the future hold for them as Google approaches its 25th birthday in September?

Alphabet, without a doubt, is one of the most successful companies of all time. Six of their products – Google Search, Android mobile operating system, Chrome browser, Google Play Store, Workspace, and YouTube – proudly boast over 2 billion monthly users. Not to mention products with hundreds of millions of users, such as Google Maps or Google Translate, and according to calculations, people spend a total of 22 billion hours daily on Alphabet’s platforms.

Since its public launch in 2004, Google’s revenue, 80% of which comes from online advertising, has grown at an average annual rate of 28%. During that period, they generated a total of $460 billion in cash after operating expenses, almost all of it from advertising. The company’s stock price has increased 50 times, making them the world’s fourth most valuable company.

With such remarkable figures, it seems hard to fathom why Alphabet isn’t performing even better. In fact, this question is well-founded and is being raised by Mr. Pichai, his subordinates, and investors. The company finds itself at a delicate moment – not solely, or even primarily, because of AI. The core digital advertising business has reached saturation, with growth in revenue becoming unstable in the double digits and increasingly tied to economic cycles. At the same time, finding new material growth sources is challenging for a company that already generates $300 billion in annual revenue. This task is further complicated by investors calling for higher cost efficiency and capital discipline, thus requiring a change in the company’s historically free-spending corporate culture.

Let’s take a closer look at Alphabet’s money-making machine. Throughout the 2010s, digital advertising seemed invincible in the business cycle. During its peak, advertisers spent like there was no tomorrow. In worse cases, they shifted some of their non-digital marketing budgets online, where giants like Google and Facebook (now Meta) offered more precise ad targeting than traditional television ads…

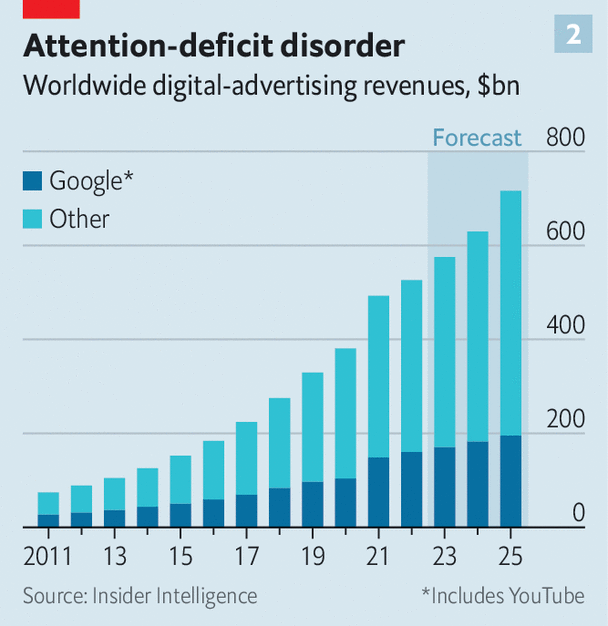

Now, with online advertising accounting for two-thirds of total ad spending, businesses have smaller budgets for non-digital advertising. Insider Intelligence, a data company, predicts that global digital ad sales will grow 10% or less annually in the coming years, down from the 20% or more in the past decade.

The slowdown last year offered a glimpse of the future that made investors fearful. Google also cannot easily capture a larger piece of the pie. Trustbusters believed their market share was too high and sued Google in the US for search monopoly abuses. Google’s deal with Apple, where they pay $15 billion annually to become the default search tool on 2 billion iDevices, has also been scrutinized closely.

Although search is still incredibly profitable, with an operating profit margin of nearly 50%, according to brokerage firm Bernstein, how people search for everything on the internet is changing. Most product searches today start not on Google but on Amazon, the e-commerce giant. According to Google’s executives, 40% of teens and young adults search for suggestions for things like restaurants or hotels on TikTok, a short video app, or Instagram, a similar app from Meta. Google may lure some of these “searchers” to its platform, as YouTube is doing with a TikTok rival app called Shorts. However, videos lack the unique revenue-generating capabilities of search boxes.

Afterward, they are also training AI on valuable web texts, images, and sounds that can serve to simulate human-generated content. Mr. Pichai’s insistence that Alphabet is a “native AI” company is correct. Most observers believe that deep pockets and abundant talent will enable Google to address technology challenges, such as the trend of “bot hallucination” or the high cost of serving responses (which Google employees are busy resolving).

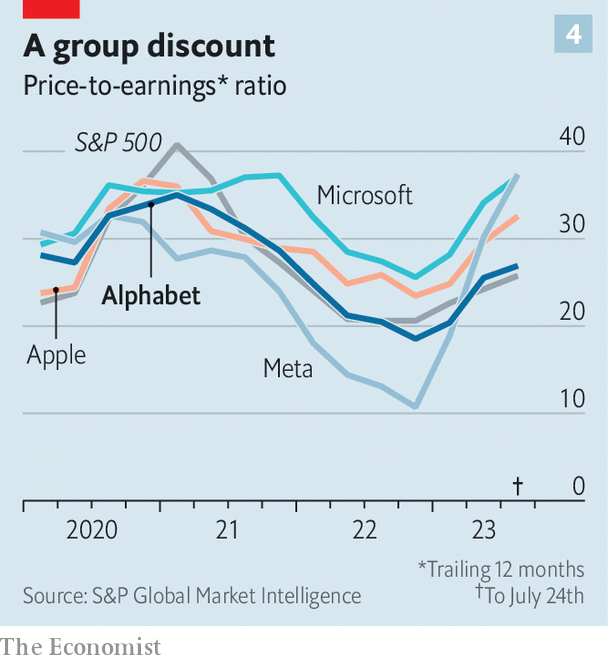

However, it still leaves the question open about how much money the bot-supporting products will actually make. Setting search aside and considering Google’s strength in creating specialized products that may not have revenue-generating capabilities, there is no reason to think that their AI segment will be any different. Despite the recovery, Alphabet’s stock price continues to lag behind Microsoft, a company that has begun earning from AI.

Google’s founders, and thanks to Alphabet’s two-tier ownership structure, the company’s lords Larry Page and Sergey Brin, have long realized that their main revenue engine will slow down at some point. They have sought ways to supplement it and, someday, perhaps replace it entirely. That’s the primary reason for the birth of Alphabet in 2015. The parent company would oversee Google along with many other projects, including self-driving cars to longevity medicine.

However, not everything has gone smoothly. From 2018 to 2022, Alphabet recorded an accumulated operating loss of $24 billion, more than six times the total revenue during that period. Other bets have also consumed at least a portion of the parent company’s capital expenditure, which amounted to $31 billion last year, and a significant portion of the annual $40 billion research and development budget.

Indeed, a more profound issue is that it is very challenging for any new joint ventures to shift the balance. Only a few industries – such as finance, government, healthcare – are large enough and uninterrupted enough to make a material impact on Alphabet’s top-line products. Conquering these markets requires massive investments for uncertain returns, and no market allows them to enjoy the near-monopoly situation with minimal capital that Google has enjoyed with search advertising.

With tougher revenue growth, some investors believe that Alphabet should focus on driving profitability by improving its overall profit margin. Many complain that Alphabet’s stock trades at a lower price compared to Apple or Microsoft, and not much higher than the S&P 500 index of large US companies in general – a disappointment for a technology pioneer.

The Economist suggests that the way to address these issues is to restructure Alphabet from the top down. For example, separating different business segments such as search, YouTube, Google Cloud, etc., would allow each business to focus resources on what they do best. Another approach would be to chart a new direction, similar to how Apple transformed from an expensive desktop computer provider to a mobile phone giant and Microsoft shifted from selling software on CD-ROMs to cloud computing. However, such a drastic move would require the consent of Brin and Page, which may not be easily achieved.

Moreover, a complete overhaul comes with significant risks. Investors and analysts remain deeply skeptical about Mark Zuckerberg’s bet on the metaverse. Apple and Microsoft themselves spent years “wandering” before finding their second lives. And radicalism is not Mr. Pichai’s style. He is smart, sophisticated, and wise. He played a crucial role in building the core business, which he even led before taking over as CEO of Alphabet in 2019. However, he may not be the visionary type who looks far into the future.

When a company reaches nearly a quarter of a century, it resembles a middle-aged person who is required to carefully consider what they eat, eliminate weaknesses, avoid risky behaviors, and maintain discipline. If these efforts succeed, according to a shareholder, Alphabet can continue to increase its profits even as overall sales growth slows down, ensuring envy-worthy profits.

However, the above approach will be put to the test, especially as AI, both a creator and a potential disruptor, continues to advance. Technology, which Alphabet clearly still owns, will not be enough to harness the potential of this technology. It will also require astute commercial acumen. Google demonstrated this early on when it developed the search advertising business model. Since then, at least in terms of business, Alphabet has been able to achieve the spectacular success of that innovation, allowing some of its commercial sinews to atrophy. If it doesn’t pivot with the advent of the AI era, there are plenty of hungry competitors craving that position.

According:The Economist